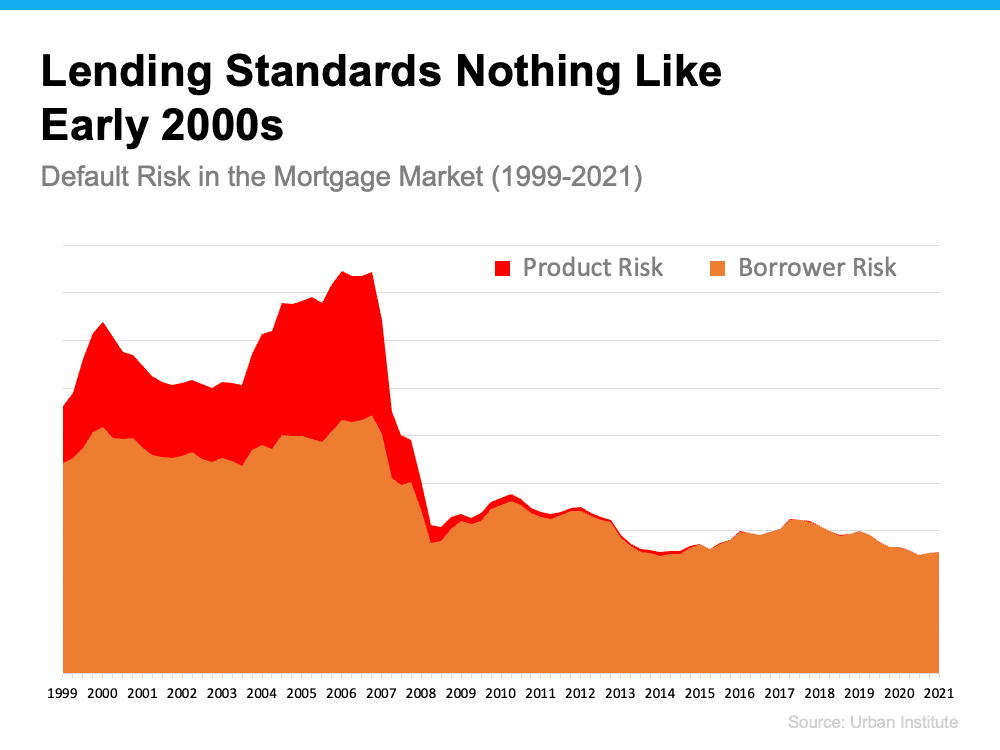

Data from the Urban Institute shows the amount of risk banks were willing to take on then as compared to now.

Today, we are in a completely different situation, especially in New York City.

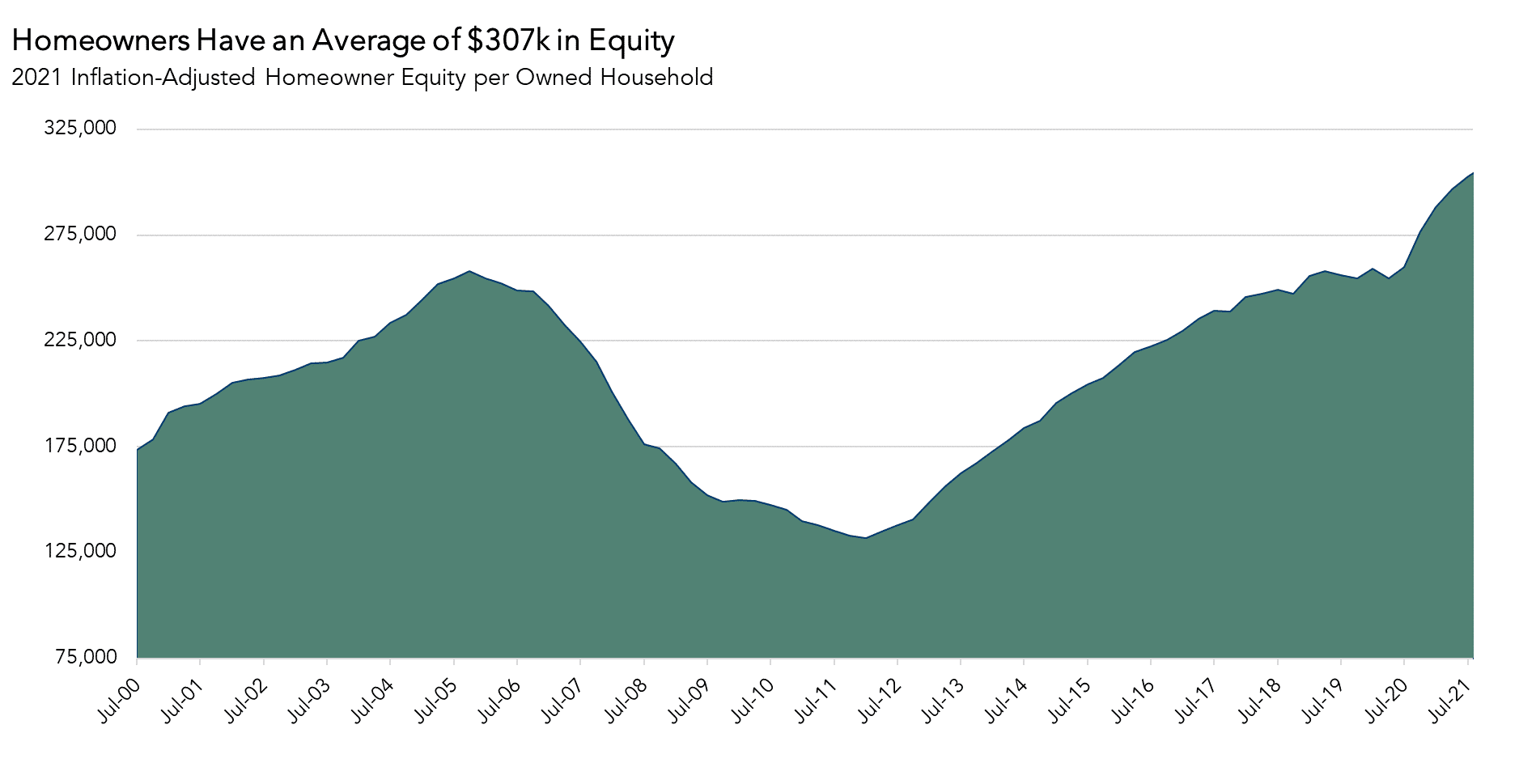

"In inflation adjusted terms, homeowners in Q4 2021 had an average of $307,000 in equity- a historic high." - Odetta Kushi

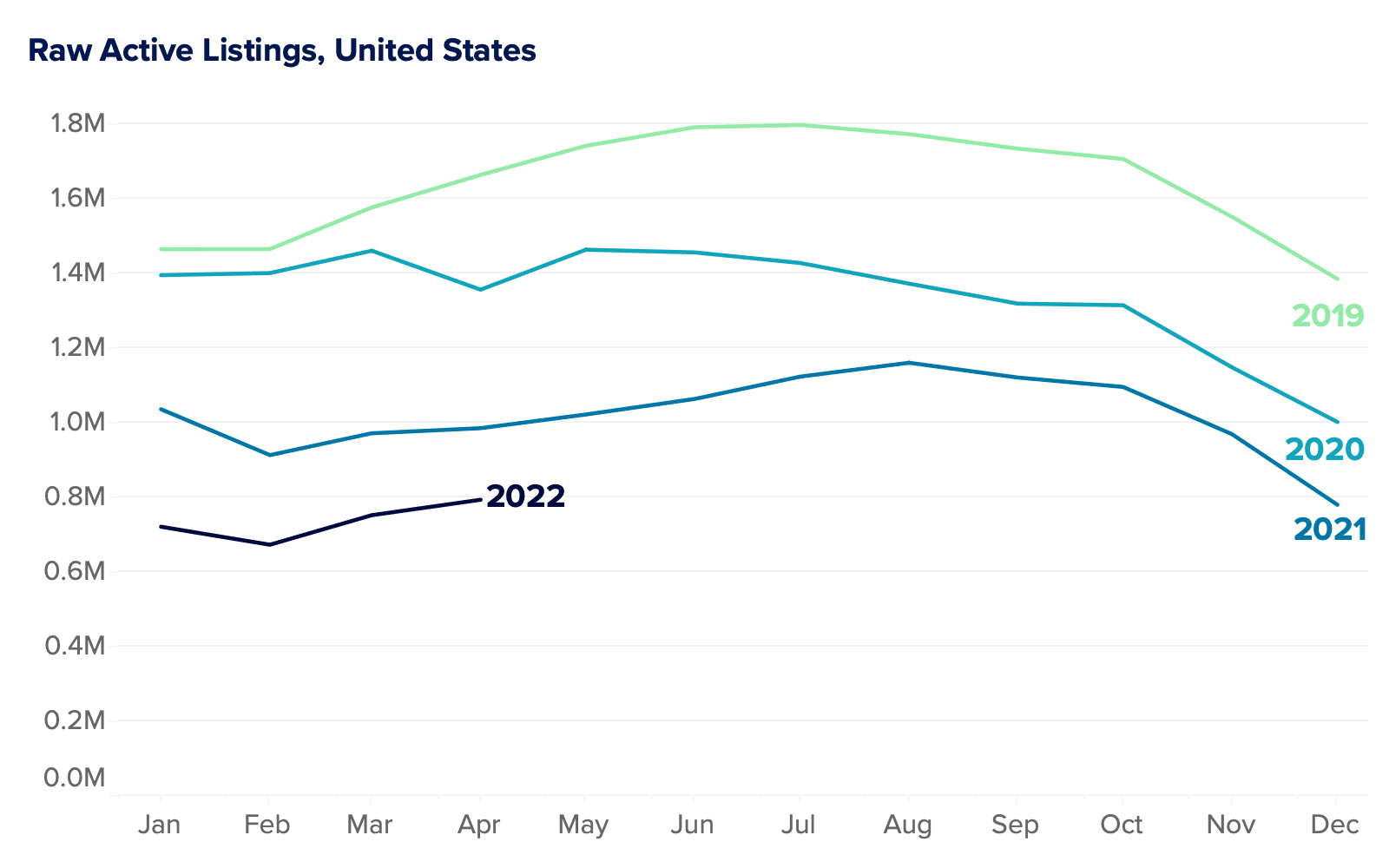

The demand is also real these days and not inflated by non-existent loan standards. Buyers are driven to buy due to genuine re-evaluation of what owning a home means, especially after the pandemic and with work from home situations.

Homeowners today also have more equity than they did back in 2006.

Homeowners didn’t forget the lessons of the crash as prices skyrocketed over the last few years. Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has more than doubled compared to 2006 ($4.6 trillion to $9.9 trillion).

The latest Homeowner Equity Insights report from CoreLogic reveals that the average homeowner gained $55,300 in home equity over the past year alone.

Odeta Kushi, Deputy Chief Economist at First American, reports: “Homeowners in Q4 2021 had an average of $307,000 in equity – a historic high.”

ATTOM Data Services also reveals that 41.9% of all mortgaged homes have at least 50% equity. These homeowners will not face an underwater situation even if prices dip slightly. Today, homeowners are much more cautious.

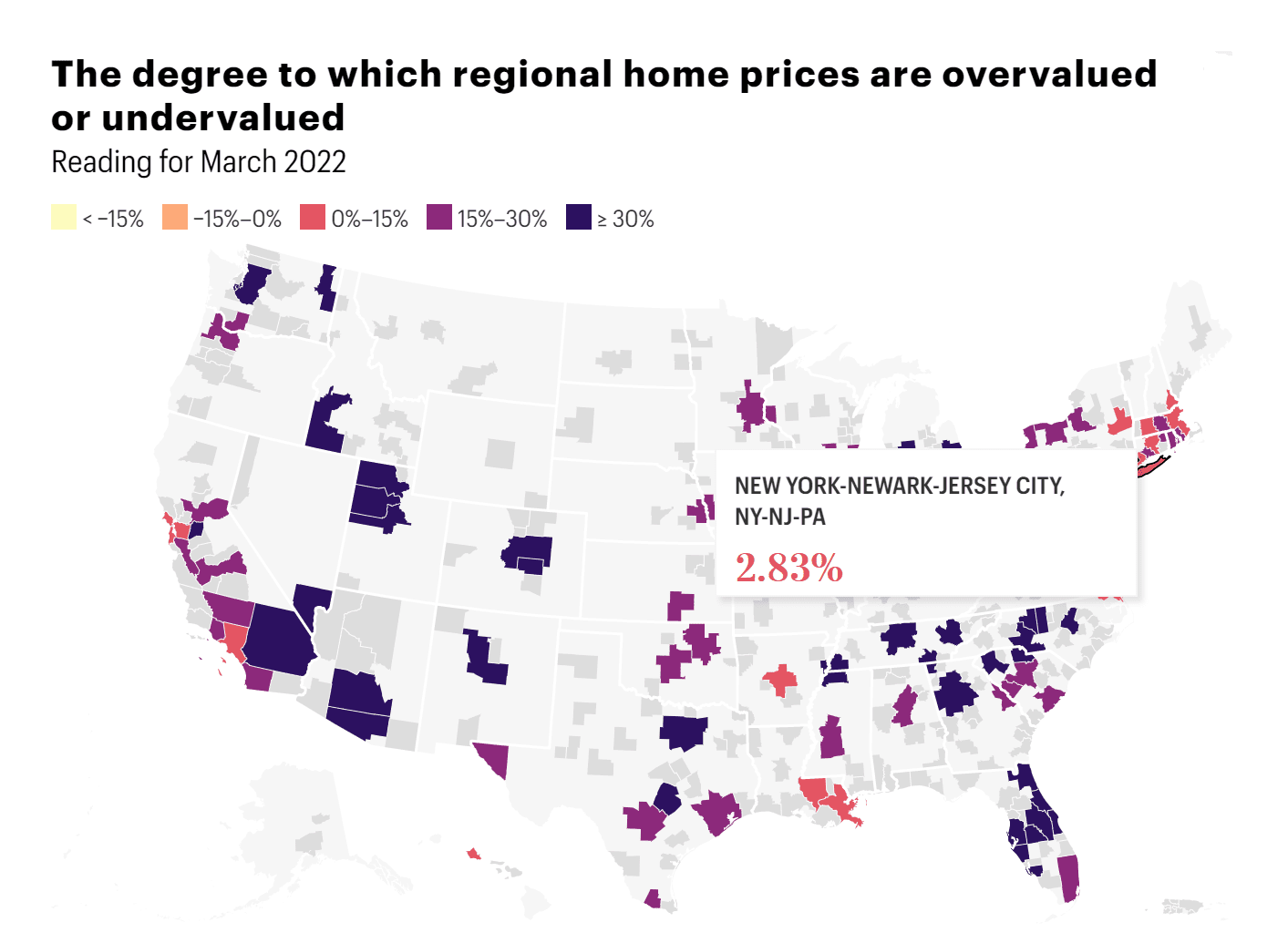

A POSITIVE SCORE INDICATES THE HOUSING MARKET IS OVERVALUED. A NEGATIVE SCORE INDICATES THE HOUSING MARKET IS UNDERVALUED.

MAP: LANCE LAMBERT SOURCE: THE REAL ESTATE INITIATIVE AT FLORIDA ATLANTIC UNIVERSITY

Any price correction coming to the city due to rising rates will not be as steep as in other locales in the nation. Not only that, but if a 2023 recession does come and employers finally have the economic power to force staffers back into the office, our housing market is at a lower risk of home price correction since we will see those employees coming back to our business centers.

Zillow has gone even further saying that all this talk of a bubble about to burst will actually make it a reality.

According to Zillow, “If prices did begin to fall, we know there are millions of hindered first-time buyers, or younger millennials soon to be aging into that situation, waiting in the wings to snap up homes if they see a bargain. Those first-time buyers will continue to feel the pressure from rising rents, which jumped 17% in just the past 12 months. And a generally high-inflation environment will keep homeownership looking attractive as a hedge against inflation.”