Watch this content HERE

Opportunities for buyers and hope for sellers? Time to say goodbye to a tough 2023 and welcome to a hopefully easier 2024! Let’s look at what NYC’s housing market did in Q4 and over the past December.

I have been saying this for quite some time now: buyers and sellers were in a tight spot due to inflation and rising mortgage rates this year. Sellers are staying off-market because they don’t want to give up the low rates they locked into a year or so ago, and buyers fall out of the race as the rising costs mean they can no longer afford to buy. This quarter, sales volume fell by close to 17% from Q3 and over 10% from the same time last year. For those who remained on the market, cash was king: all-cash sales made up two-thirds of all quarterly sales – a new record.

Supply is short, dropping 13% from last quarter and over 15% from last month. We are also at the lowest point of supply since late 2016. The lack of available inventory has kept the median and average sales price high, with increases of about 5% from last quarter on both. These numbers are the highest they’ve been since 2018 – before the pandemic.

Contract activity is still underperforming the historical average for December, but in a quarter-over-quarter view, we see a 5% increase from Q3 and over 7% increase from the same time last year. This upward trend highlights positive movement as we enter 2024.

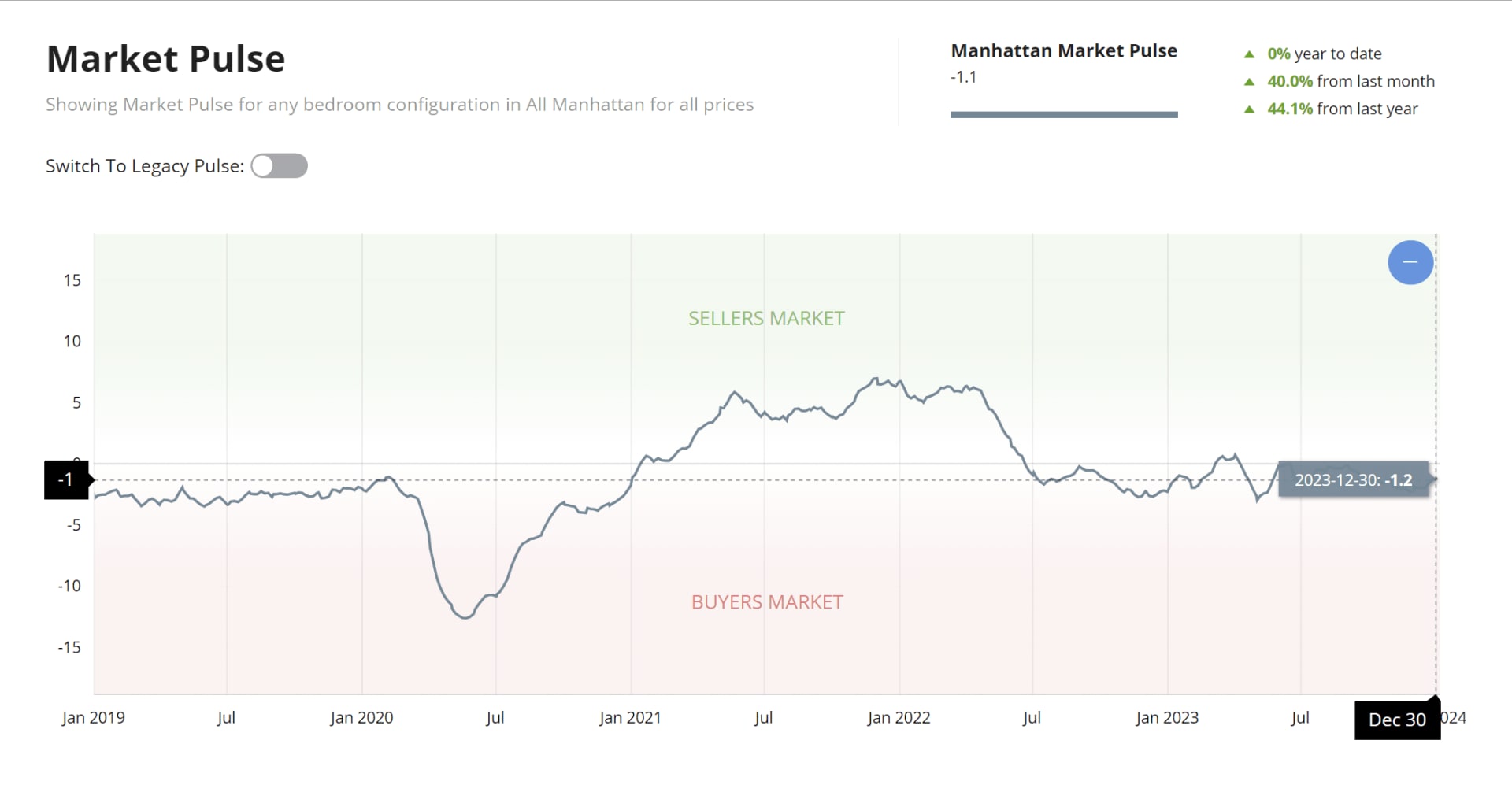

Looking at the market pulse, we have been in a buyer’s market for a year and a half. We are now seeing the numbers rising by 40% and up from last month and last year. For buyers, the past 18 months or so have really been a long window of opportunity despite the lack of listings, and it’s been a long stretch. If you’re a buyer interested at all in buying in the next 6 months you need to consider the competition coming your way– more ppl will list in the upcoming months.

Just look at the optimal time to list chart as your indication: where today you may have 1 or 2 people seeing the same listing as you, in 2 months you may be up against 6 other buyers. The leverage window is likely to change once we get into March.

Now let’s put the market into context. Average 30-year mortgage rates closed out 2023 at around 6.22%. This is just 20 basis points higher than the start of 2023 before the Federal Reserve hiked the rates and pushed mortgage rates up to their highest amounts in the last 20 years. Most housing market predictions for 2024 don't predict us going below 6%, but mortgage rates have already dropped faster than what major forecasts expected. So, it's possible we could finally see rates drop into the 5% range this year. This will likely jump-start the market. Sellers who have been waiting will return to the market and buyers who were priced out will come back with affordability easing. And with increased activity, you can also expect competition.

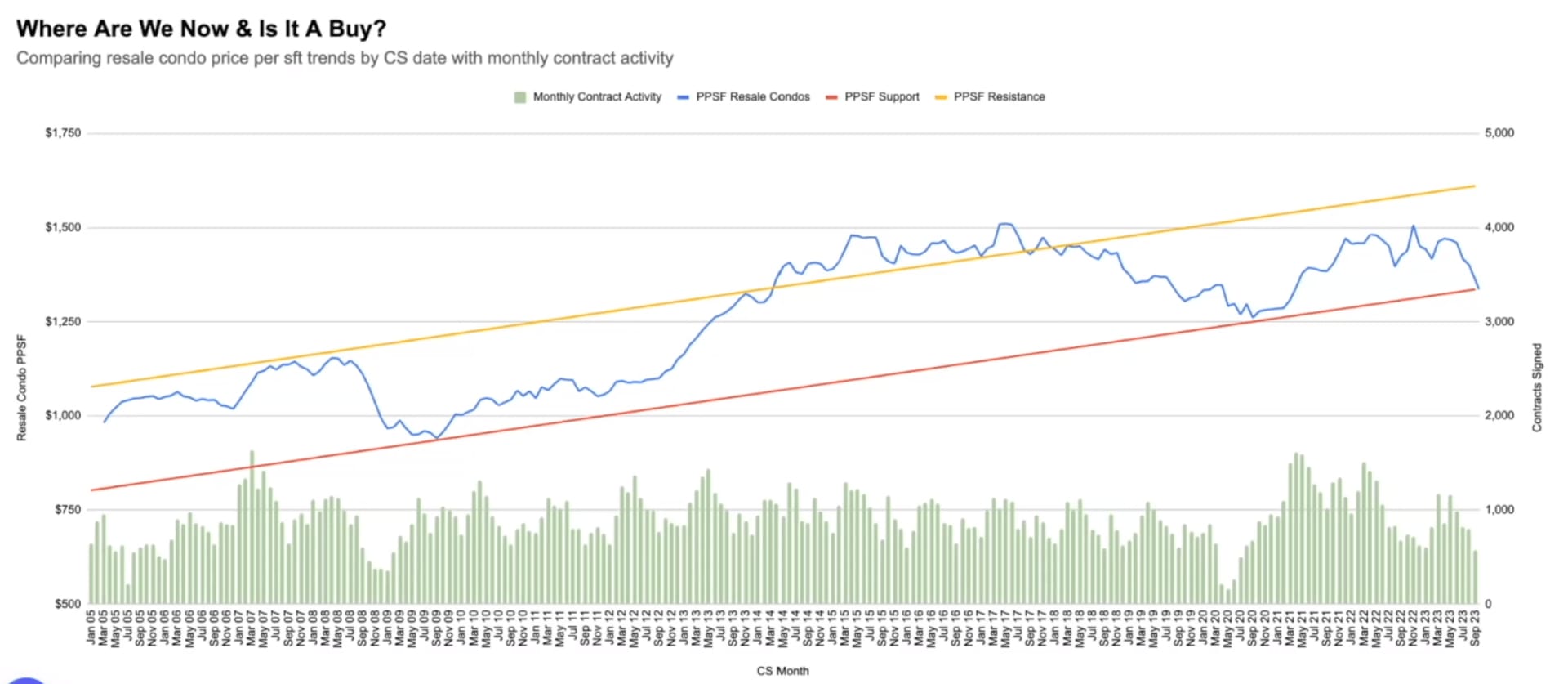

Comparing price trends with monthly contract activity, we are nearing the lowest point – November-December that are still to come will probably be lower – but this downtrend happened already. The likelihood of us going up in PPSF is higher based on the past. Once volume comes back there is a rebound in price point.

Buyers who are looking for deep value and higher-than-average negotiability need to look at listings that have been on the market for over 170 days – the average days on the market for Q4. These sellers chose to stay in the market, they probably have to sell, and likely did a price cut already. On the Compass website, there are currently around 4,000 active listings in Manhattan that have been on the market for over 170 days. The value for money is here.

---

So, my bottom line? We will see the market recover in the next 6 months or so. Rates will ease, buyers will come back, and with them – sellers who have been holding off. The transaction environment will change as we will see more competition and the leverage will gradually shift from buyers to sellers as the market moves toward recovery.