It is March and have you heard the news? NYC’s housing market is turning the corner as we speak! Let’s dive in!

Buyers are experiencing a different market than sellers right now; let's sort out the confusion: the source of it is whether you look at price activity based on closed deals or based on contract-signed deals. Right now PPSF is reflecting the bottom of the “dip” since it looks at deals that were signed 4 months ago – this is price data by sold listings, and this is what buyers normally look at. If we switch to looking at prices based on contract signed date – a measure sellers will most often use since that is how their brokers price a listing: units going into contract – we have a different story to tell. Here we see a bump in the market and more support for the seller side. So how you look at different data to measure the same thing matters and can cause confusion.

Let’s talk about the numbers:

Last week was the biggest week of the year so far in terms of supply, with over 400 listings coming to market. This is a good pace although it is slightly lower than last year. We are also finally starting to see a positive trend in net inventory: new supply is higher than contract-signed and off-market listings put together. Buyers, you can finally look forward to more inventory this spring season! And although this rise in inventory is more shallow than normal, we still hope it doesn’t translate to fewer signed contracts as a result. It will take March through June to reach peak inventory, and supply will first have to come into the market before contracts get signed.

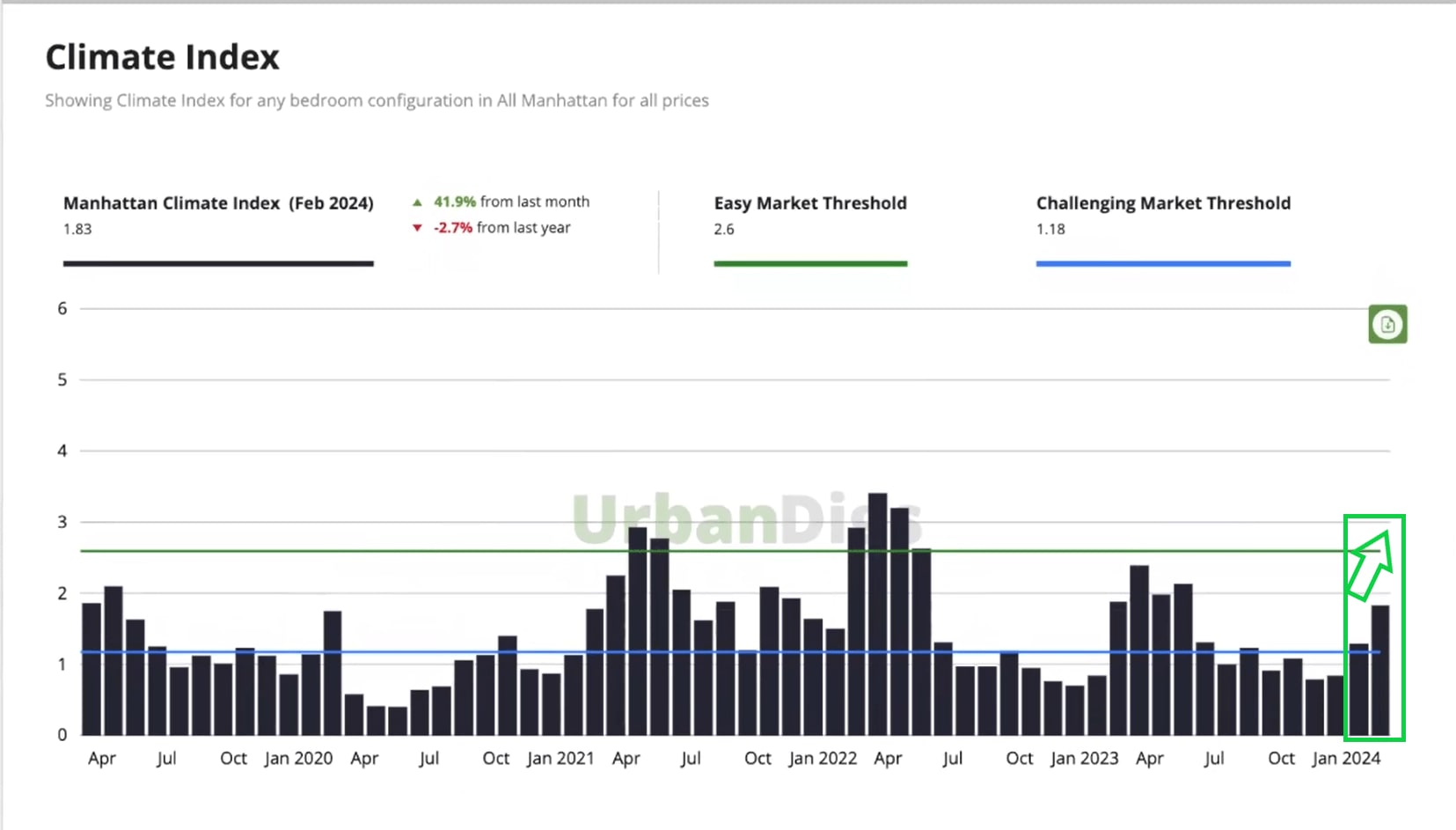

About interest rates: Although there is a 97% chance the Fed is pausing its interest rate cuts and 50% chance it will cut rates for the first time in June, the climate index is in recovery after 7 months of a challenging environment.

Now where it really gets exciting is contract signed activity: liquidity pace is on the rise, staying above 2019-2020 levels but still tied with 2023. We have a way to go but can still call it a success.

---

Bottom line? For the first time in a long time, the market is more rewarding to sellers. Buyers who are still looking at 4-month-old data have expectations that may not line up with what sellers are expecting, giving each side a different view of the market. With a rising, much healthier market, hopefully, we can meet in the middle.