Watch this content HERE

2022 was truly the tale of two worlds, with a strong first 6 months, leading to a slowdown in the second half of the year. What happened in Q4 in 2022 and where are we heading?

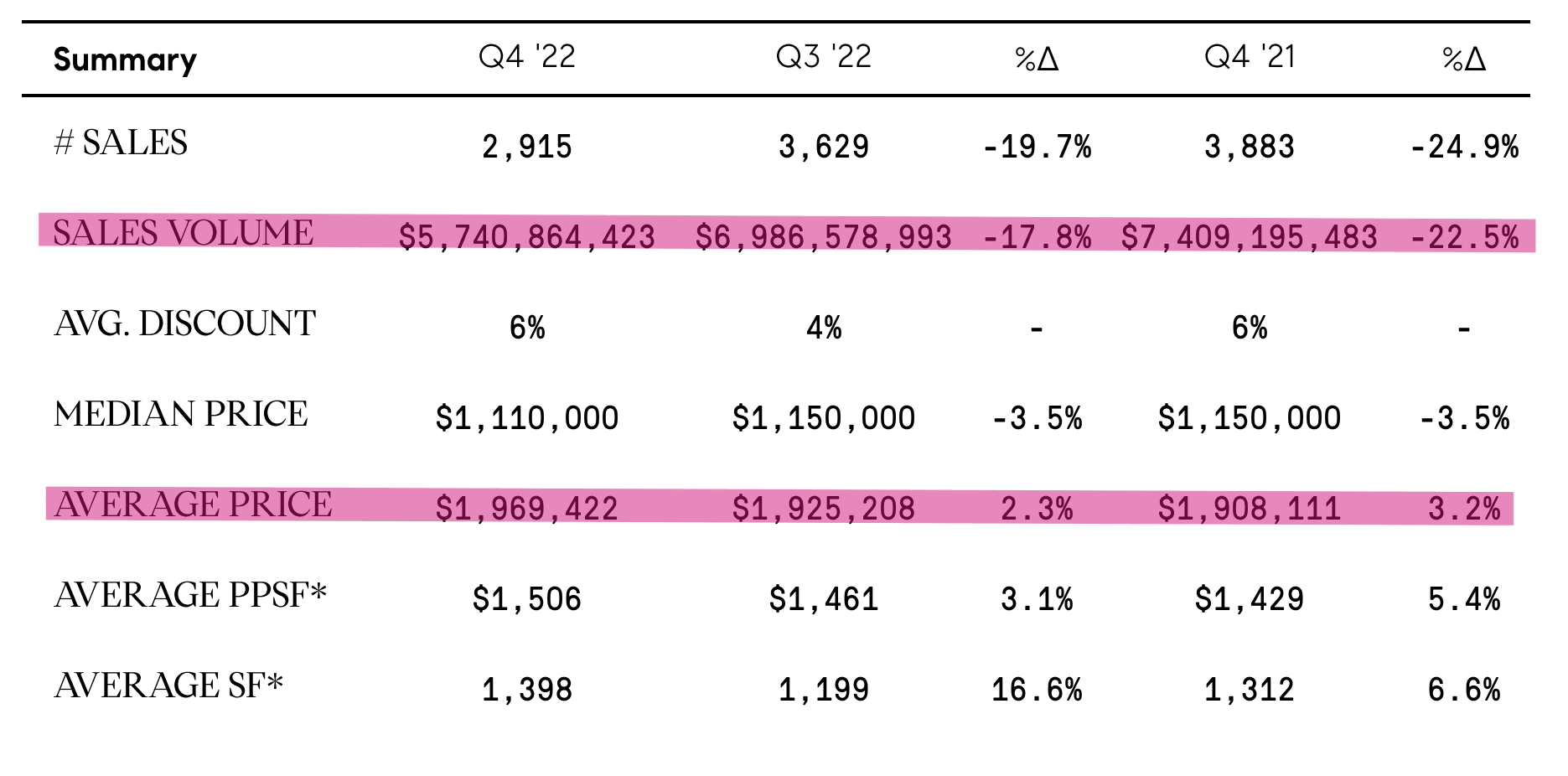

In 2022, more apartments sold in the city than in all but 3 years since 2012. In the 4th quarter of 2022 dipped 22.5% from last year and almost 18% from Q3, But the for close to $2,000,000- a 3% increase compared to the previous year.

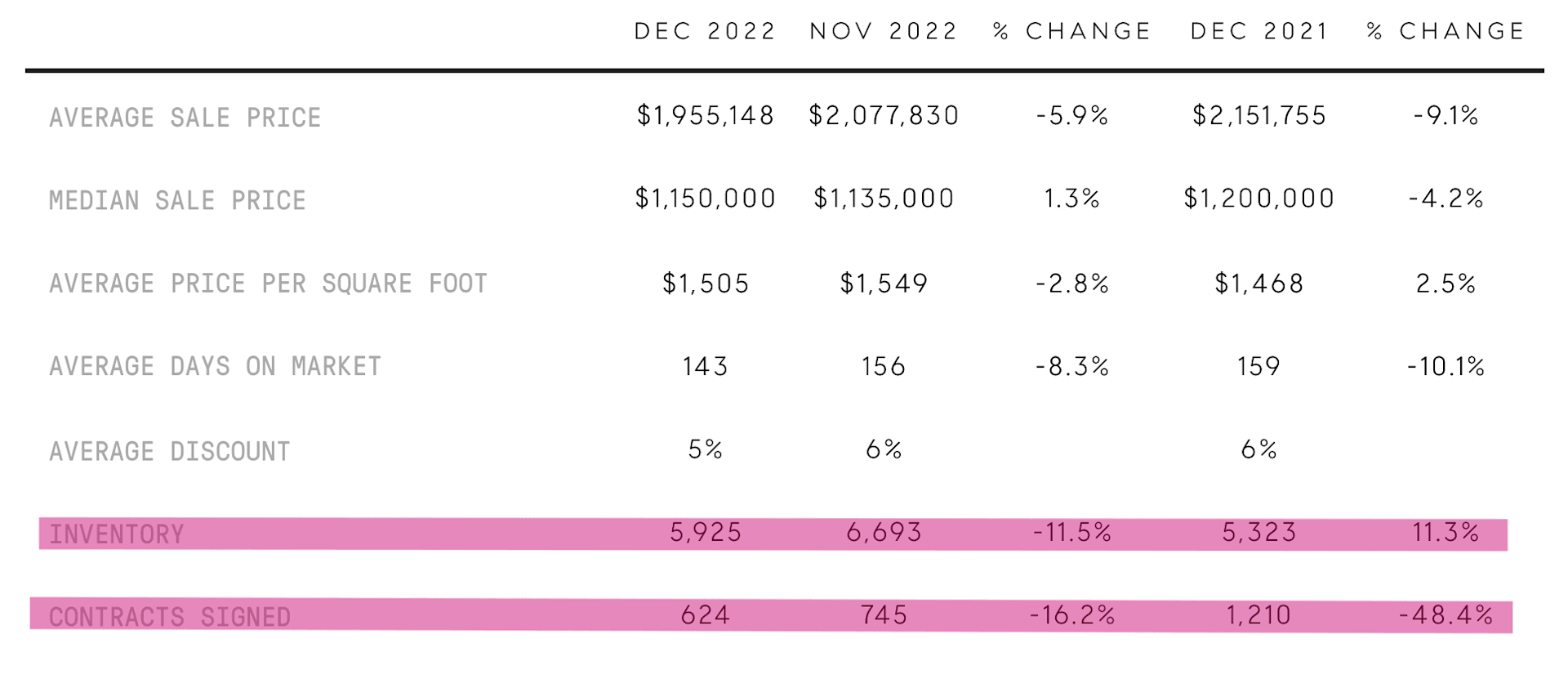

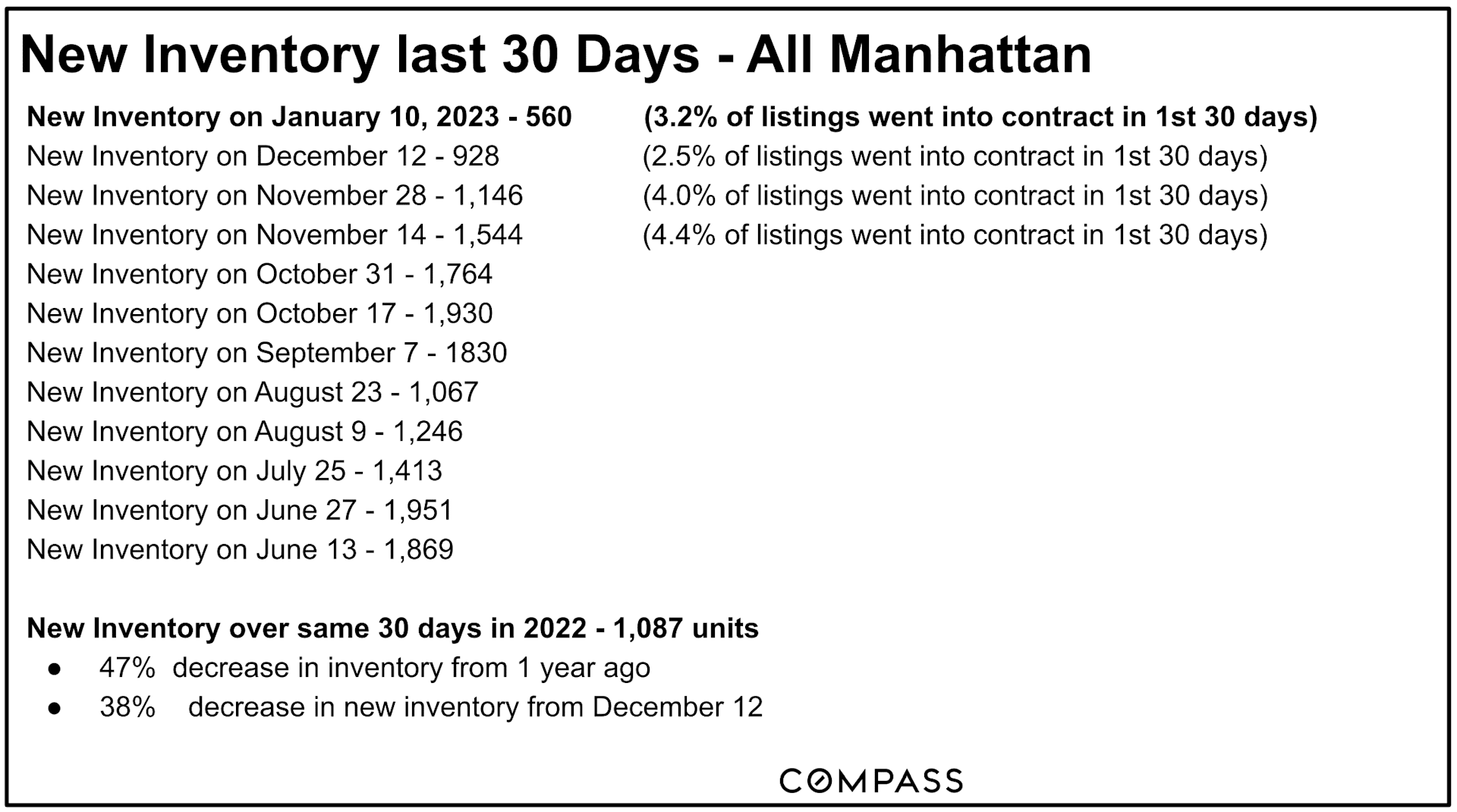

December is usually the best month for buyers and worst month for sellers, it is quiet, people are spending the holidays away with their families and buying a home is not a priority. This December we saw an 11% drop in new listings and 16% drop in contract signed activity compared to November.

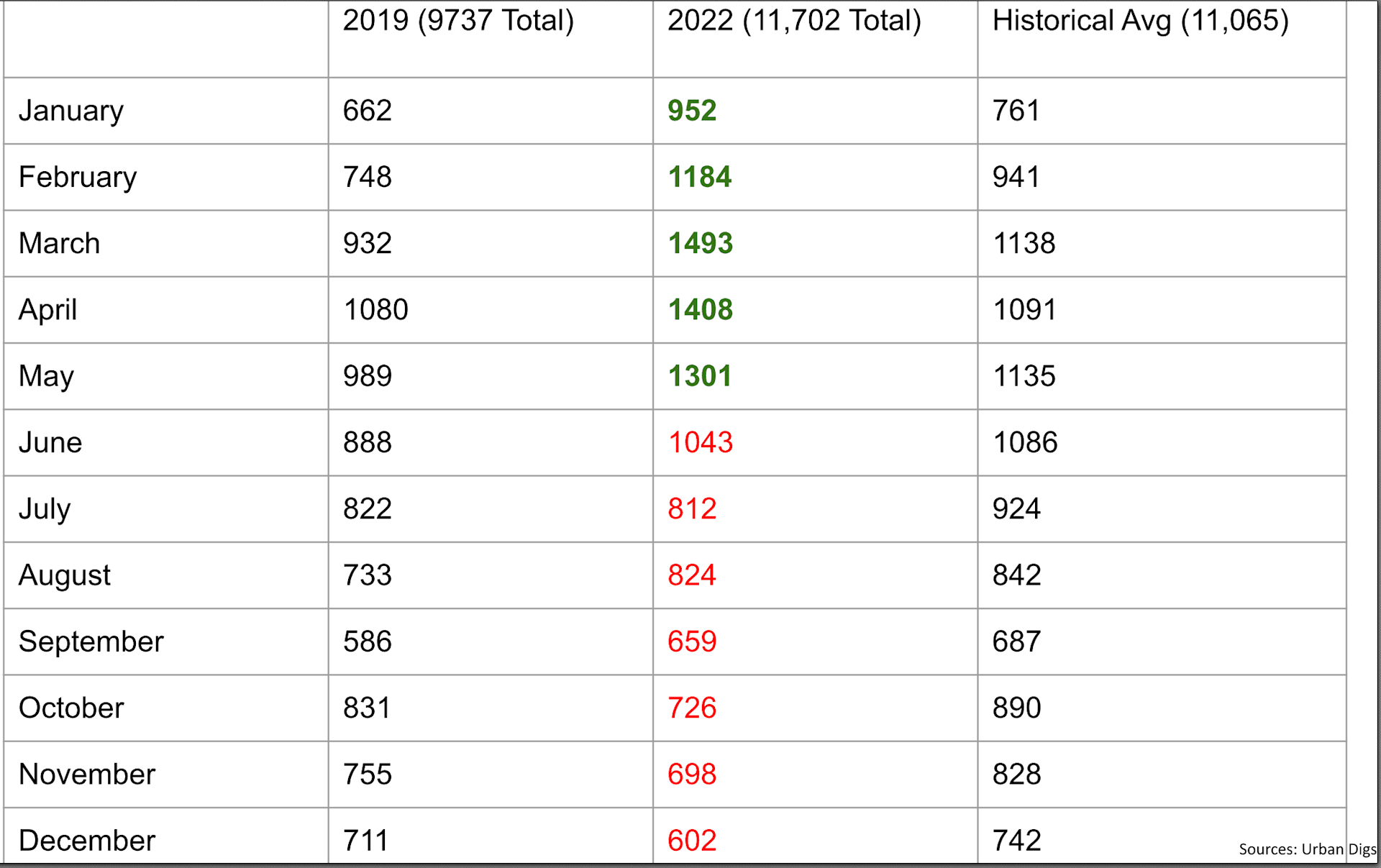

Overall, the last quarter of 2022 saw the largest sales decline since the third quarter of 2020, during the height of the pandemic. We saw a peak of activity in the first 6 months and a drop since June till the end of the year mainly because of the spike in interest rates. Looking at contract signed activity month by month in 2022 vs. 2019 and historical averages, we see a strong start to the year, and an ending below historical averages, but still close to 2019 levels.

Let's compare 2022 stats to those of 2019, a better year to look back on than the abnormally strong 2021 or the slow, covid-stricken 2020:

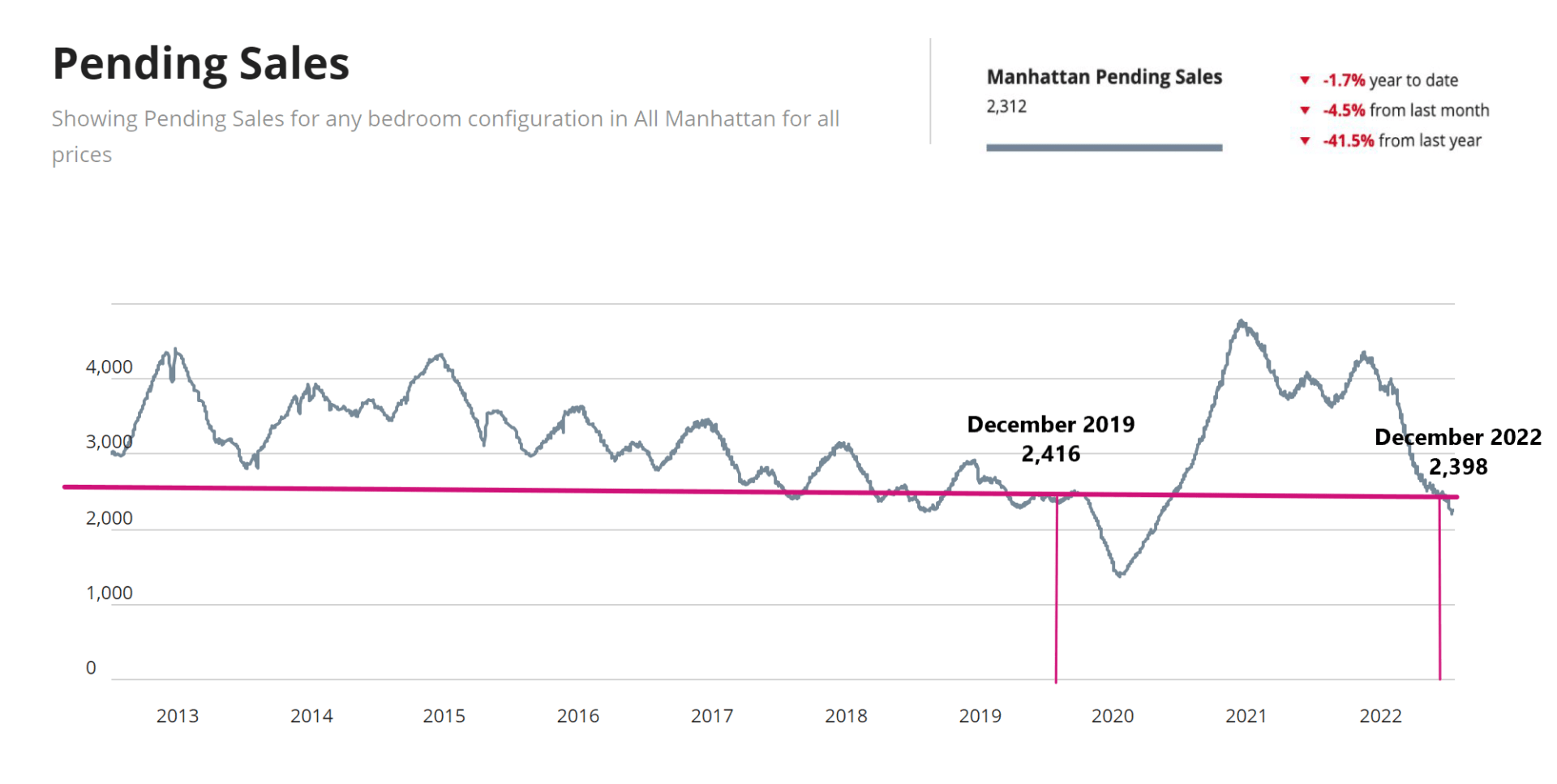

When we zoom out to look at the last 6 months of 2022, the market resembles the activity we had in 2019. In December 2019 we had 2416 pending sales, this December we had 2398 pending sales.

Source: UrbanDigs

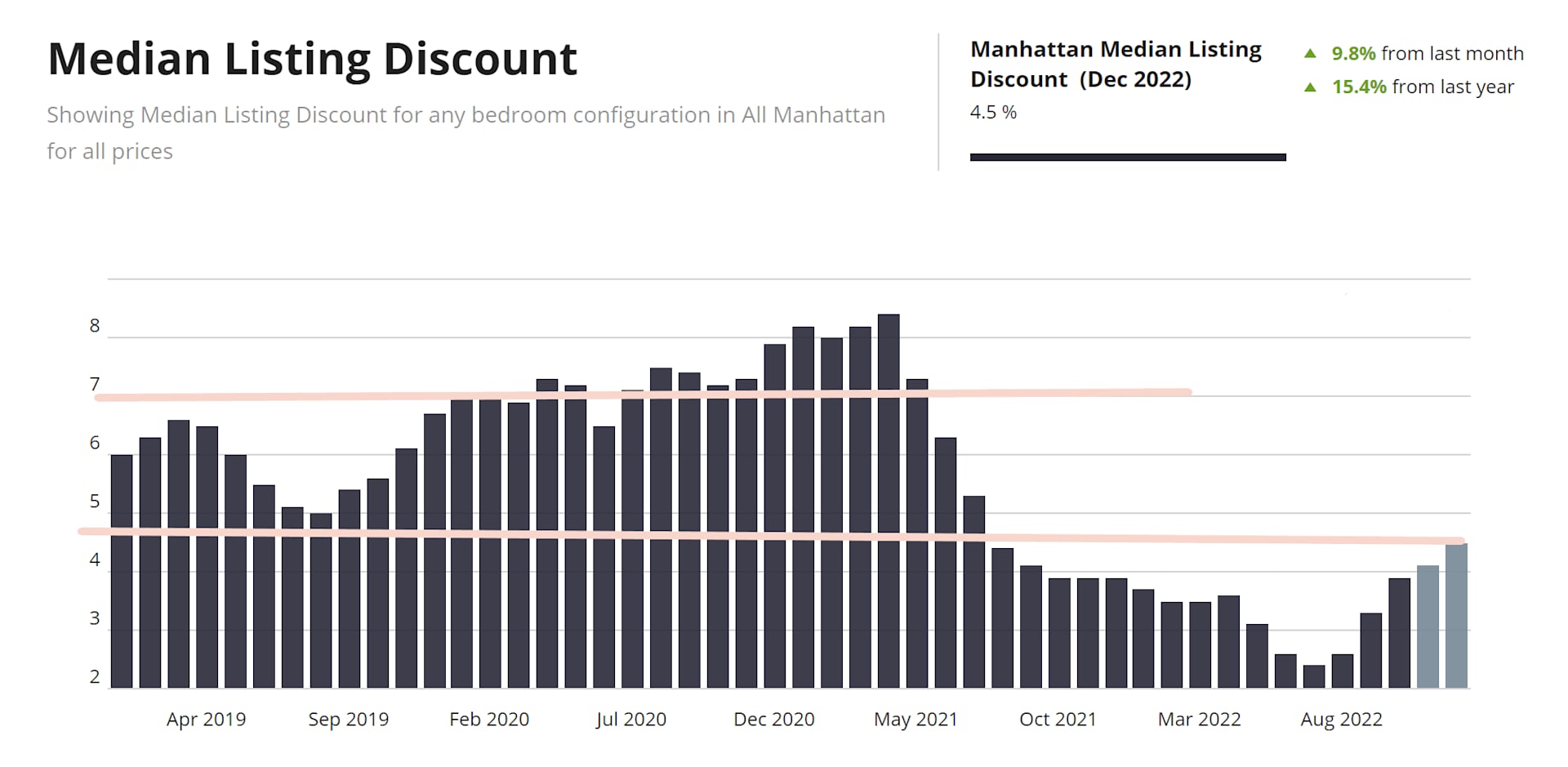

Supply level was the same as well, but it took longer to sell in 2019 than now: Average Days on the market in 2019 was 90 and in 2022 properties sold within an average of 76 days – a tight market. Another interesting statistic to look at is listing discount: in 2019 we saw 6-7% listing discount, compared to a high of only 4.5% in 2022.

Source: UrbanDigs

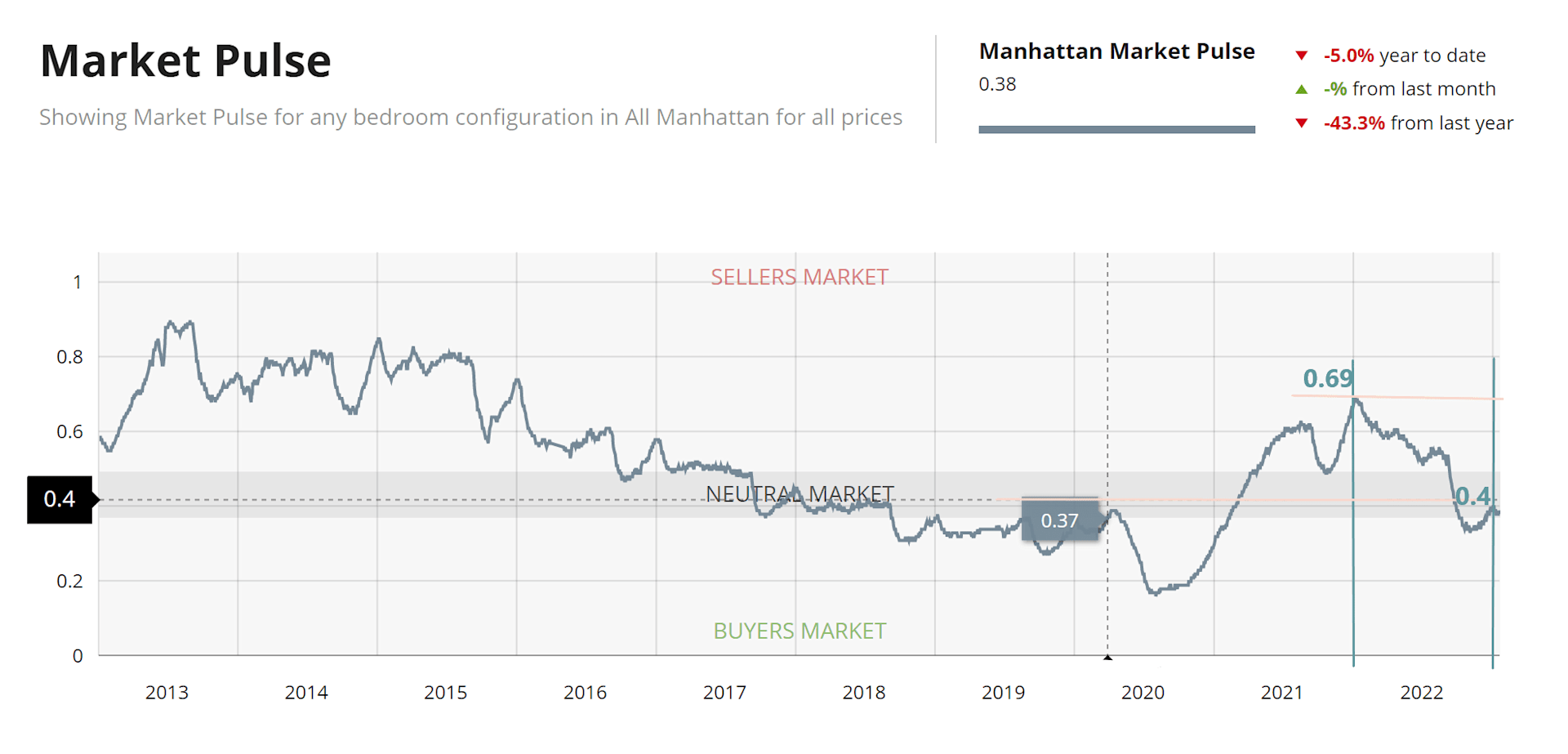

The market pulse in early 2019 was 0.37 and ended with 0.36- a fairly static, strong buyers’ market. In 2022 the first 6-month market pulse was 0.69 - seller’s territory, but the year ended with 0.4, a buyers’ market once more.

Source: UrbanDigs

So where are we heading in the new year?

The 2021 frenzy to buy apartments in has died down, and 2023 will be a year with pockets of opportunity. January is always the month we see a bump in buyers and indeed we saw 59% increase in people who visited open houses on the first week of January, compared to mid-December. In Manhattan alone, that increase was as high as 115%!

New inventory is 48% down from a year ago. When we see this low activity for so long, sellers start to drop prices and the market shifts, giving buyers an opportunity to find a good deal. But as soon as we reach 2019 numbers again and hit a static point, sellers will raise prices again. We will see bigger listing discounts until that stabilization. Many people are currently on the sidelines, but they can only hold for so long. Interest Rates have dropped and if this will continue, we expect to see 2023’s contract signed activity similar to 2022 only flipped, starting slower and then picking up. If I were a buyer, I’d be out there shopping right now.