People from all over the world have always been drawn to New York City's real estate for its prime position as one of the world's main financial, cultural, and commercial centers. But whether you're buying or selling in NYC as a non-US person, there are a few things you should know.

First,

How Do We Classify Who’s a Us-Person and Who Isn’t?

The tax code (for our purposes of residential real estate) defines three basic classifications of individuals and foreign corporations:

- US Persons: Includes any US citizen anywhere in the world, Green Card holders anywhere in the world, US corporations, US partnerships (even if all members are foreign), Any alien individual who passes the “Substantial Presence Test”. If any of these conditions apply, then such a person is a US tax resident. Generally, it does not matter if such person is also considered a tax resident in another country, and any non-citizen/ non-Green Card holder who spends excessive amounts of time in the US (generally more than 120 days every calendar year) is likely to be considered a US tax resident.

- Non-Resident Aliens: Includes Any non-US citizen/ non-Green Card holding individual who does not pass the substantial presence test, Foreign Trusts, Foreign Corporations/ entities, and Foreign Partnerships.

- US Domiciliary: This is a subjective criteria that only applies to non-US citizens. It analyzes various factors such as time spent in a place,

where you work, have a home, family life, etc. Having a Green Card is a strong factor but not a a determining one, and undocumented persons can be considered a US domiciliary.

Here Are 3 Things Foreign Buyers Should Consider:

- Taxation - Nonresidents should consider a holding structure like an LLC to mitigate tax impact. It’s a bad idea to purchase US real estate in your own individual name because you may have Estate and Gift tax issues later on.

- Privacy - Foreign buyers usually come from places where the real estate they own is private and assume it’s the same in the US. You should be aware that real estate holding is public information in the USA.

- Closing Fees - Most foreign buyers don’t know there are usually higher closing costs in NY like the Mansion Tax or Title Insurance costs-- we always explain these upfront to avoid surprises.

Gift and Estate Taxes

Gift and estate taxes apply to transfers of money, property and other assets. Simply put, these taxes only apply to large gifts made by a person while they are alive, or large amounts left for heirs when they die. The current federal exemption of up to $11.5M per person (set to expire in Jan 2026 and revert to approx. $6M). Any amount above $11.5M is taxed at a rate of 40% of fair market value of asset at date of death. Non-Citizen/ Non Domiciliary are only taxed on US-based assets, but have a much lower exemption of only $60K; any asset above $60K is subject to federal estate tax of up to 40%.

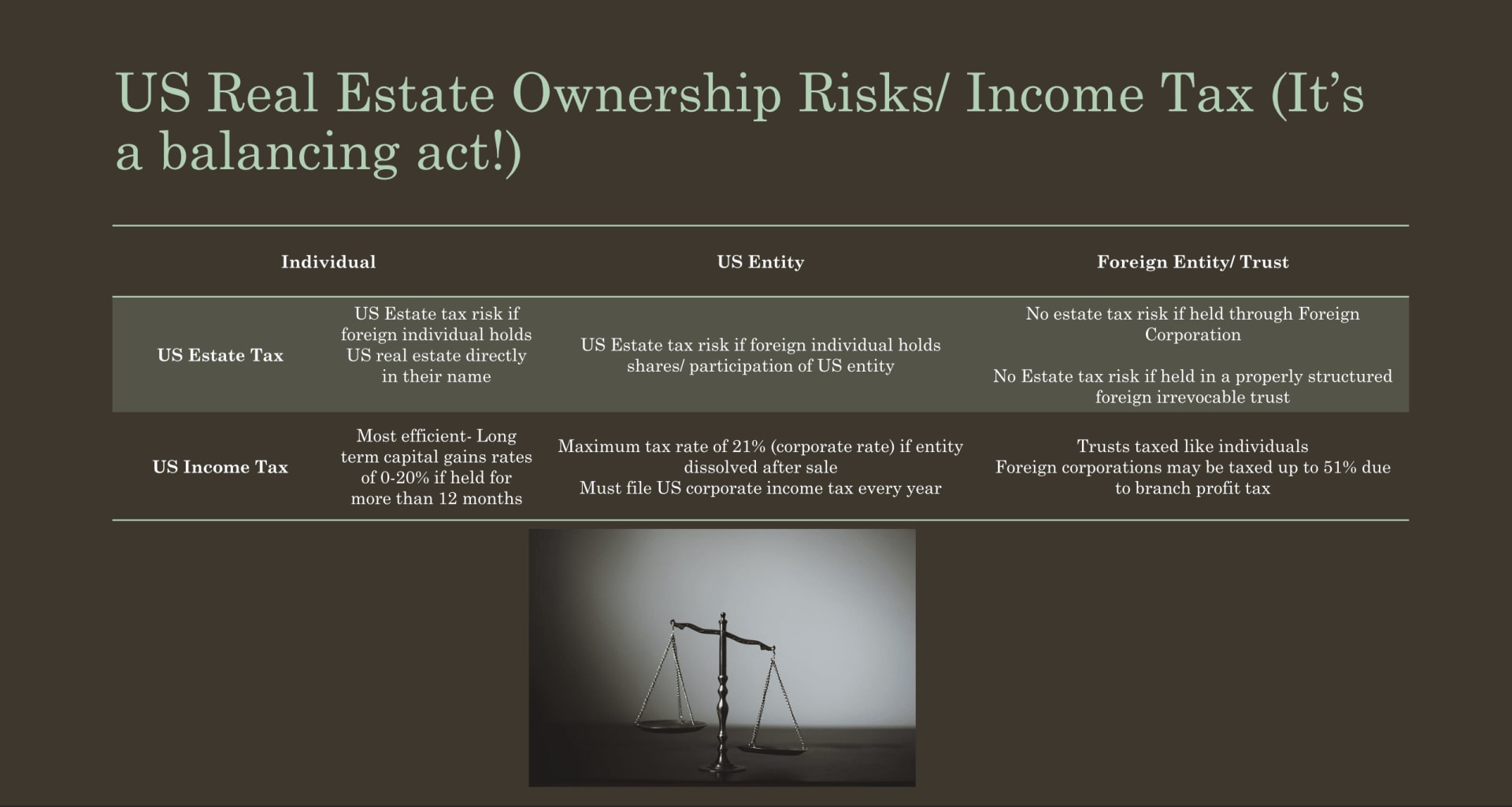

Take a look at this table, showing the tax risks of US real estate ownership:

For non-US persons, here are a few common options for holding structures:

• Holding in individual name: Creates a US estate tax issue and lacks privacy, but is the most efficient holding structure for US income tax purposes (usually done for lower value real estate with a life insurance to cover US estate tax);

• Holding directly in an irrevocable trust that avoids US estate tax and is more income tax efficient (but problematic for clients that live in jurisdictions that don’t recognize trusts, and is a potential for home country gift tax);

• Holding directly in the name of a foreign entity (works to avoid US estate tax, but is not income tax efficient, and would require FIRPTA withholding at sale)

• Holding in the name of a US Corporation wholly owned by foreign entity

Here Are 3 Things Foreign Sellers Should Consider:

- FIRPTA Withholding - Foreign sellers will see a 15% withholding at closing (which is the FIRPTA Withholding); you should know this well ahead of time and discuss to see whether an exception can be applied.

- 1031 Exchange - If you’re looking to use funds in a 1031 exchange, FIRPTA still applies! Foreign sellers should discuss ways to resolve any future issues with their attorney.

- Power of Attorney - Many foreign sellers don’t plan to be at closing, so any power of attorney or corporate resolution must be prepared well in advance as it may require apostille or a trip to the local US consulate.

What is FIRPTA withholding?

FIRPTA is an acronym which stands for Foreign Investment in Real Property Tax Act. It applies whenever a non-US person transfers interest from real property in the US. The withholding requirement in that case is 15% of the sale price and it is NOT the tax you owe for the sale; it is a mechanism to ensure the IRS receives payment. Withholding must be sent to the IRS within 20 days of closing and is the buyer’s liability for unpaid tax and penalties if there is a failure to withhold it or to send in the withholding in a timely manner.

You can try the following strategies to potentially avoid FIRPTA withholding:

• Purchase in a multi-level corporate holding structure utilizing a US corporation as the owner of the US real estate

• Purchase utilizing a US partnership entity (e.g. LP) or LLC with more than one member

• If already in the name of an LLC with a single member, add a member (could be small participation)

• Purchase in the name of a US domestic trust or convert foreign trust to a domestic trust (seek professional advice - rules are tricky!)

• If real estate is owned by a foreign company, consider selling shares of foreign company

So remember...

Planning must be done BEFORE closing!

• Once the deed is made into your individual name it becomes difficult and costly to restructure.

• As a foreign Owner, you will not be able to gift any interest in real estate or add additional parties to the deed without incurring US gift tax.

• If you're a foreign Owner and want to add persons to the deed with yourself (e.g. joint tenancy with rights of survivorship) without such other individuals having contributed to the purchase, it could be considered as if you've made a completed gift at the time of closing, and be subject to US gift tax.

• A transfer to a trust would be difficult, as most transfers are gifted, and would require a sale.

• A transfer to a foreign entity after closing would require recognition of gain and FIRPTA withholding to complete the transfer.