Watch this content HERE.

It is December, the year is almost over, and we are about to enter the winter market after an atypical, slow fall. What did NYC’s housing market do in November and what are my predictions for 2024?

New Inventory has dropped almost 10% from last month, which is typical as we enter the holiday period. This number is expected to drop again and pick up around mid to late January. Inventory is static and there are not a lot of options for buyers out there.

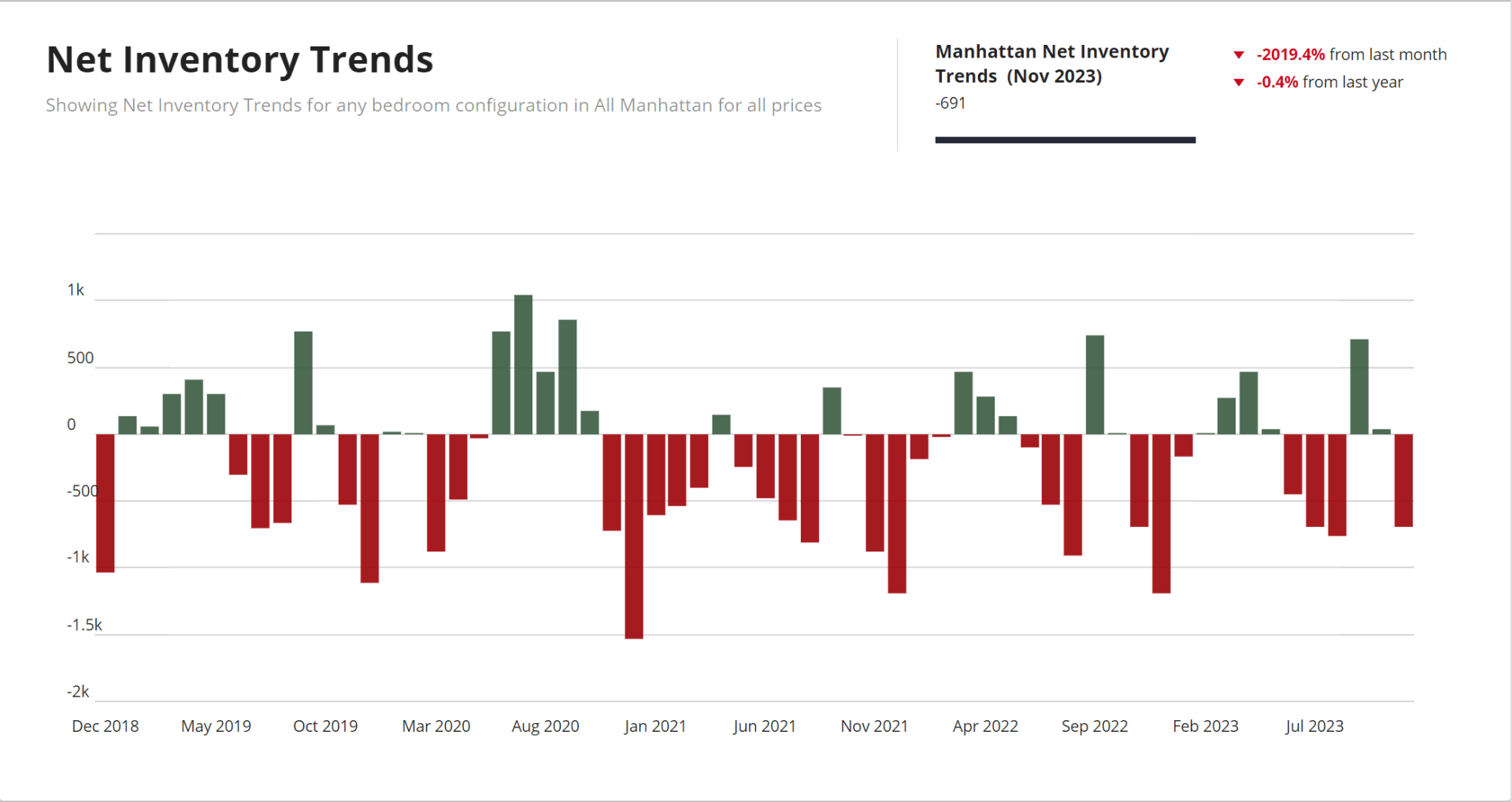

Pending sales have gone up impressively from last year but if we look at the last few months, they have been going up and down in small amounts – confirming the market is stagnant. When we look at net inventory, it continues to nosedive as sellers remove listings from the market, listings go into contract, but no new listings come back in. Again, a slow, stagnant market.

Liquidity pace, which indicates demand, is showing a deviation from historical trends to the down-side and is 5.5% lower than last month. This is a weak number, indicating a low transactional environment. This gives buyers a very big advantage over the sell side.

PPSF has gone down in the last 4 months and is almost 9% lower than last year something we haven’t seen in a long time.

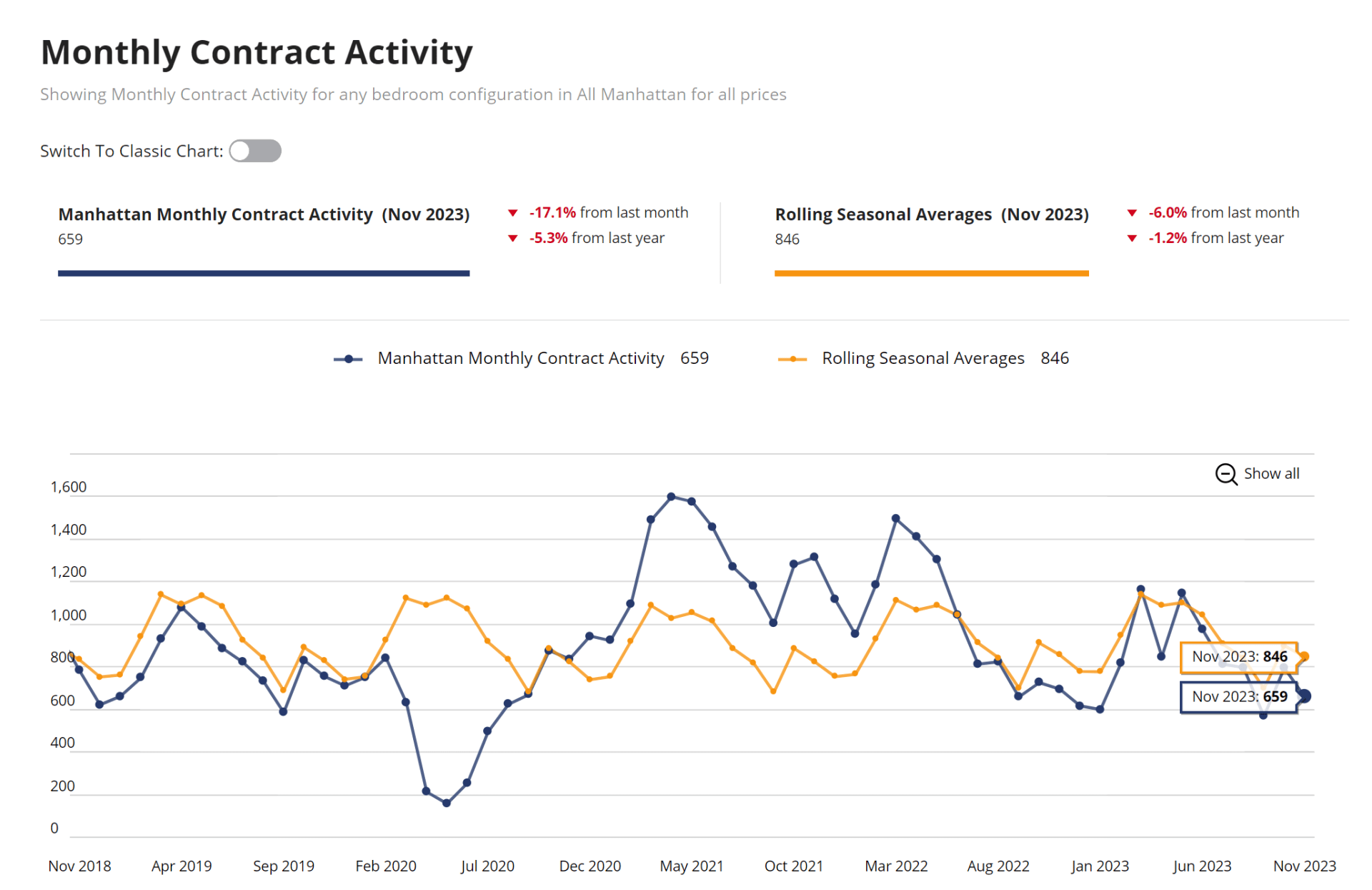

Contract signed activity is down compared to historical averages and it looks like December will be the same considering the pace we are currently transacting weekly. November was one of the worst months we’ve had with much lower contract activity than normal. If December also underperforms, we will be in the 20th consecutive month of a down market.

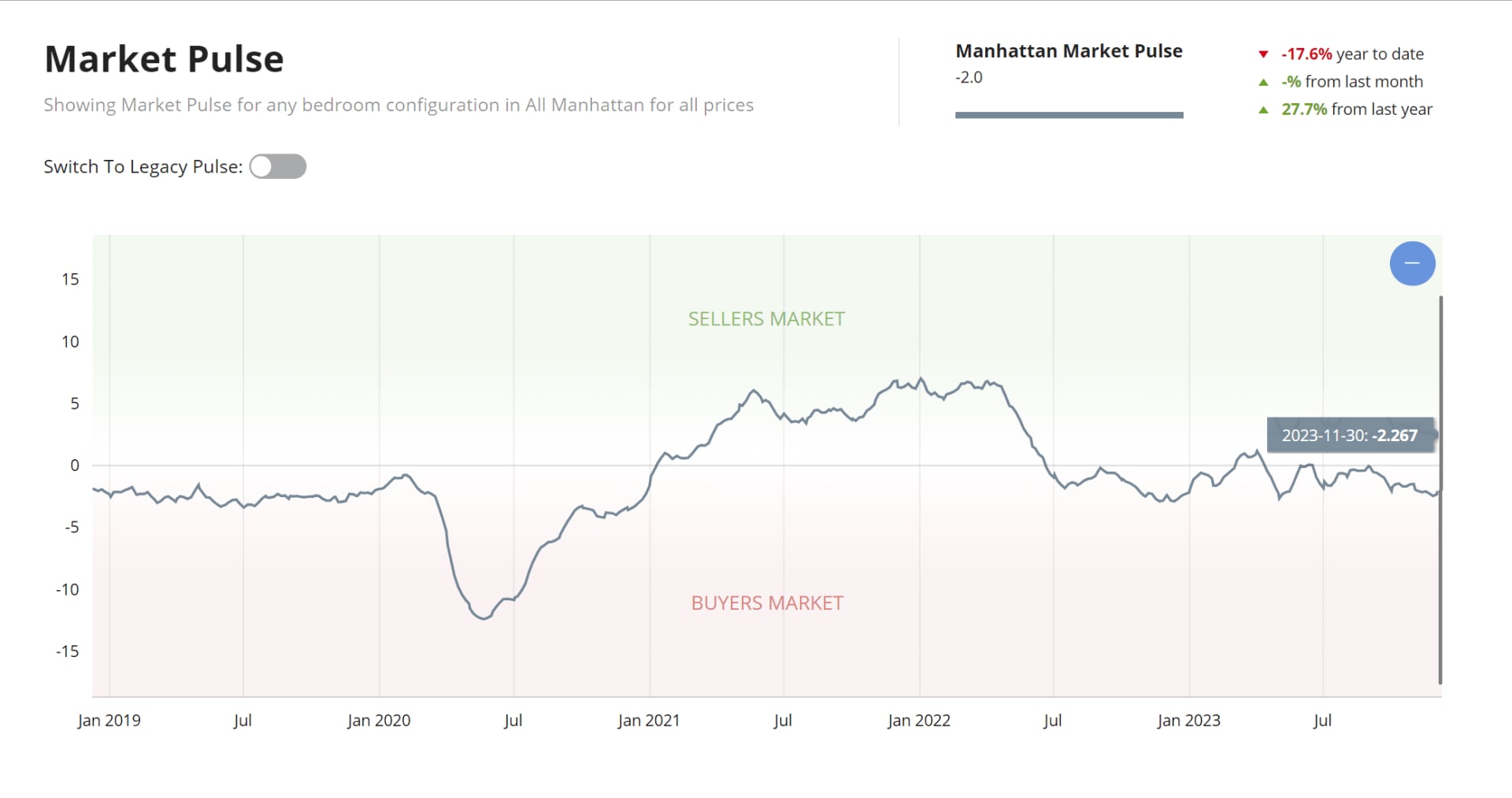

Liquid market pulse is down, year to date. It’s been a buyers’ market for the majority of the last 17-18 months.

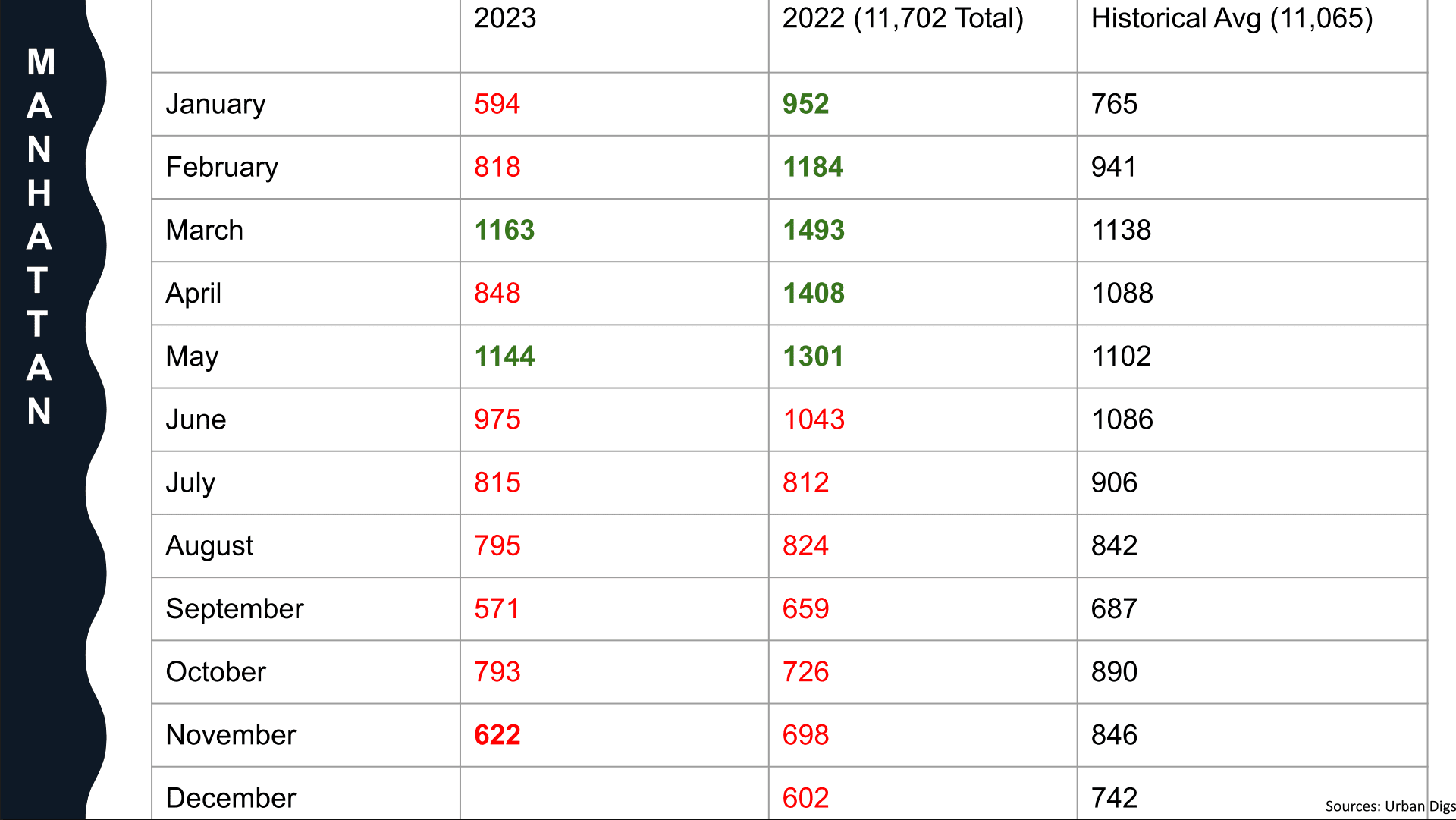

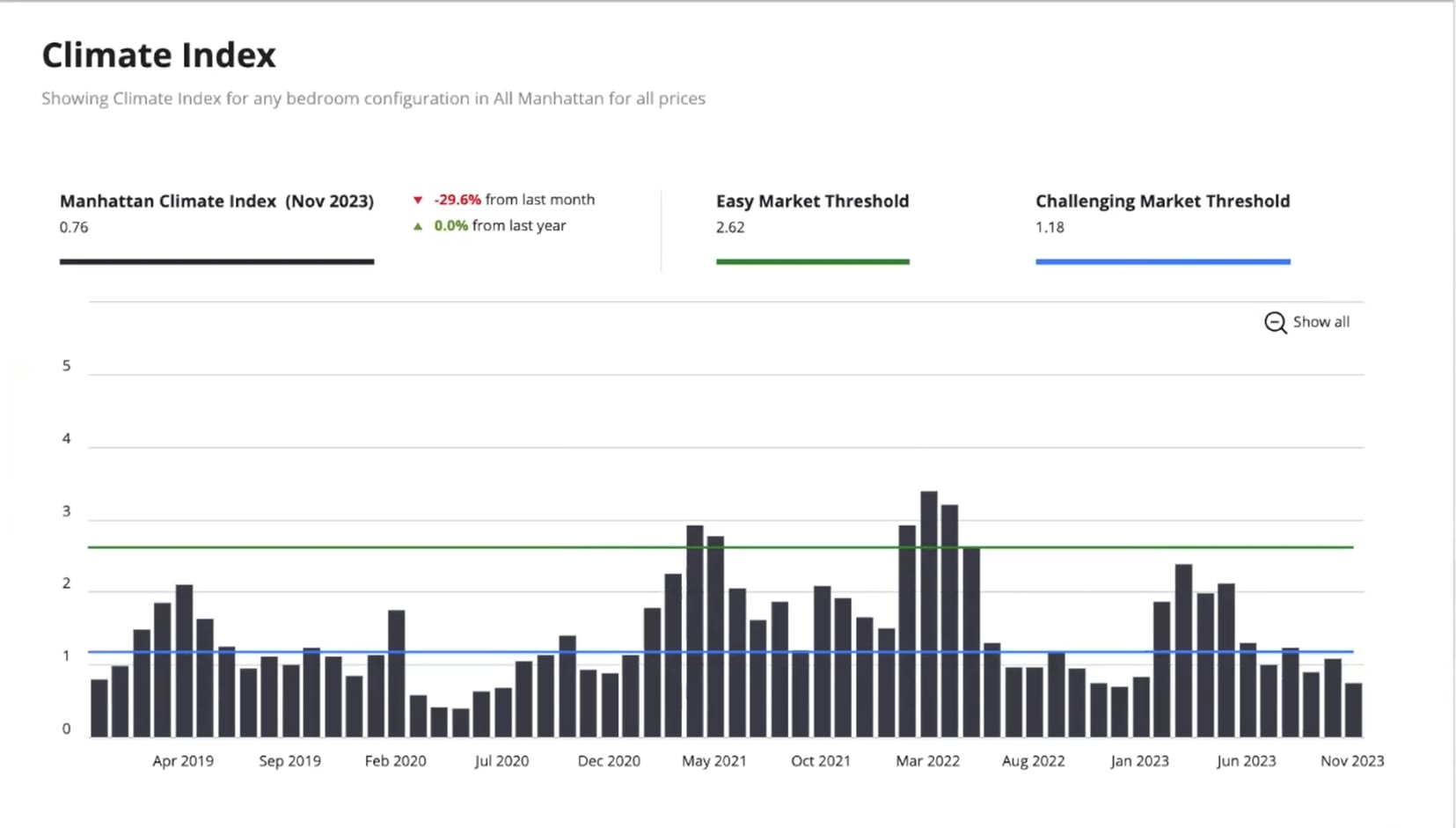

The Stars are aligning in terms of buyer leverage: climate index shows 6 months below the challenging listing environment. PPSF is down, monthly contract activity shows the slowest November since 2014, and one of the lowest in 20 years. Buyers – this is your incentive: prices are coming down and nobody’s buying. The only downside? When sellers don’t get the prices they want, they go off-market. And it’s true to ask what good is a buyer’s market when the options are slim. But as a buyer, it’s a good time to see what’s out there at least. And if you’re a seller, you should have your eyes set on the spring market and not be rash. If you have to sell, know the market you are getting into – it is not a friendly seller environment.

Here is what we predict for the upcoming months and 2024:

External factors have a huge impact on the real estate market, inflation is slowing down, and although the Fed doesn’t expect to lower its rates anytime soon, the market data suggests that we may see lower interest rates by March. Until then, it is likely that the market will stay slow.

Looking at the job market and stock market, financial conditions seem to be easing, and banks may have an easier time lending. StreetEasy also predicts that sellers will need to adopt a competitive pricing strategy, as the pool of would-be buyers will remain limited. The beginning of the year is expected to start slow, but we do expect that spring will bring back some buyers who have been sitting on the sidelines, and with it – competition.