Watch this content HERE.

I’m going to be honest, now that the first quarter of 2024 has come to an end, our market is recovering, but not thriving.

Last December, the Fed pivoted on interest rates and we were all starting to see New York City’s real estate market waking up. We had high hopes for spring but mortgage rates ended up finishing the quarter higher than in Q4, with the next Fed rate cut maybe happening in June, and even that is only a 50% chance.

And so, the spring season is losing a little steam, but it’s not all bad news: we do see positive trends, just not as high as we had hoped. In the first quarter of 2024, Inventory has reached pre-pandemic levels with 6,000 active listings in Q1, mirroring inventory levels during Q1 2019 and slightly below the average between 2014 and 2019. In addition, there was a 27.5% increase in new listings compared to Q4. These are encouraging signals as inventory rises in the spring buying season, and more sales allow for more inventory. 30-day supply is actually above the seasonal average and is slowly increasing, right on trend.

Pending sales were climbing by 9.3% in Q1 compared to Q4 and 1.7% year-over-year. 30-day contract activity is up but below where it’s supposed to be this time of year.

The combination of slower demand and rising supply is putting pressure on the market pulse which is now neutral - not favoring either buyers or sellers.

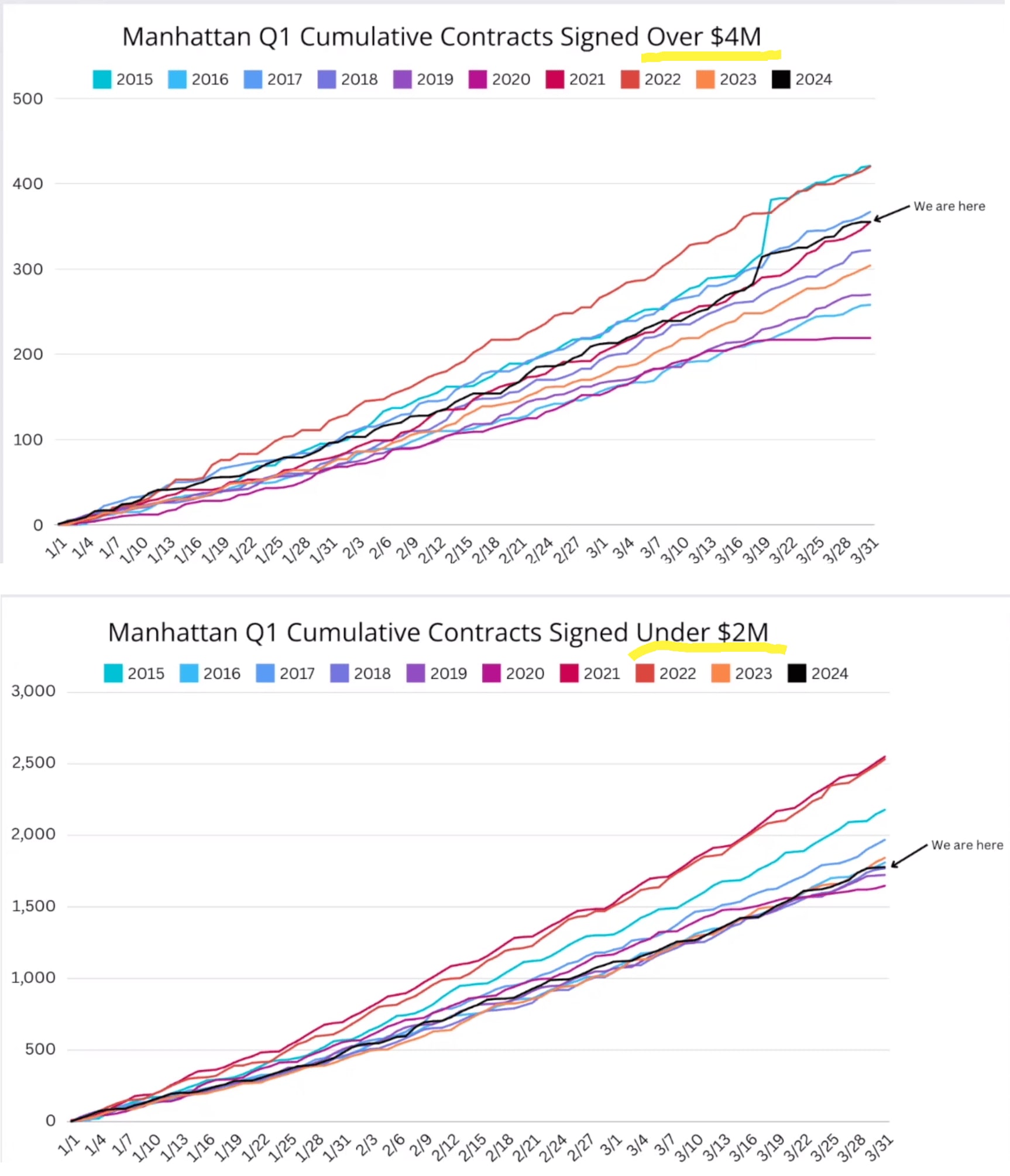

As far as price action goes, prices are stabilizing but not rising steeply. Over the quarter, condo prices declined while co-op prices rose. The luxury market continued to do well - Deals signed over the last quarter in the over $4M market we are in the top sector of the past decade. Under $2M is unfortunately a mirror image – the bottom quarter in the past ten years. Over Q1, Buyers, tired of waiting on the sidelines, showed significant interest in ultra-luxury apartments priced above $20 million, with a 140% surge in contracts signed in this category. Of course, a major factor is cash liquidity – the lower price point buyers are a lot more affected by the mortgage rates and many choose to sit the market out until we see more affordability.

Some good news for my Upper East Side audience: the neighborhood outperformed other sub-markets, with contracts signed improved by 15.5% over last year, and the median price climbing 16.3%.

Right now the market climate has gone down, and it feels like we are in 2018 or even 2019 again. We are expected to end the year at a 4.5% or so interest rate. This may postpone some of the demand and the seasonality may be disrupted by the Fed’s move.

I hope contract activity will also pick up in April; until we get to average or above listing success and an easy market threshold, the market won’t feel super active. We are basically waiting for the spark to light up demand and ignite our market.